DXC Technology (DXC) Q3 2023 Earnings Call Transcript – The Motley Fool

Image source: The Motley Fool.

DXC Technology (DXC 3.40%)

Q3 2023 Earnings Call

Feb 01, 2023,

Contents:

- Prepared Remarks

- Questions and Answers

- Call Participants

Prepared Remarks:

Operator

Ladies and gentlemen, thank you for standing by. My name is Brent, and I will be your conference operator today. At this time, I would like to welcome everyone to the DXC Technology third quarter fiscal year 2023 earnings conference call. All lines have been placed on mute to prevent any background noise.

After the speakers’ remarks, there will be a question-and-answer session. [Operator instructions] Thank you. It is now my pleasure to turn today’s call over to Mr. John Sweeney, head of marketing and investor relations.

Sir, please go ahead.

John Sweeney — Vice President, Investor Relations

Thank you. And good afternoon, everybody. I’m pleased that you’re joining us for DXC Technology’s third quarter fiscal year 2023 earnings call. Our speakers on the call today will be Mike Salvino, our chairman, president, and CEO; and Ken Sharp, our EVP and CFO.

This call is being webcast at dxc.com. Investor relations webcast includes slides that will accompany this discussion today. Today’s presentation includes certain non-GAAP financial measures, which we believe provide useful information to our investors. In accordance with the SEC rules, we provide a reconciliation of these measures to the respective and most directly comparable GAAP measures.

10 stocks we like better than DXC Technology Company

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and DXC Technology Company wasn’t one of them! That’s right — they think these 10 stocks are even better buys.

*Stock Advisor returns as of January 9, 2023

The reconciliations could be found in the tables in today’s earnings release and in the webcast slides. Certain comments we make on the call will be forward-looking. These statements are subject to known risks and uncertainties, which could cause actual results to differ materially from those expressed on the call. A discussion of these risks and uncertainties is included in our quarterly report on our Form 10-K and other SEC filings.

I’d now like to remind our listeners that DXC Technology assumes no obligation to update the information presented on the call except as required by law. And with that, I’d like to introduce DXC Technology’s chairman, president, and CEO, Mike Salvino. Mike?

Mike Salvino — President and Chief Executive Officer

Thanks, John. And I appreciate everyone joining the call today, and I hope you and your families are doing well. Today’s agenda will begin with an overview of our strong Q3 results, where our execution drove record bookings along with margin, EPS, and free cash flow that all exceeded expectations. Next, I will discuss our transformation journey and how it has helped us drive these strong results.

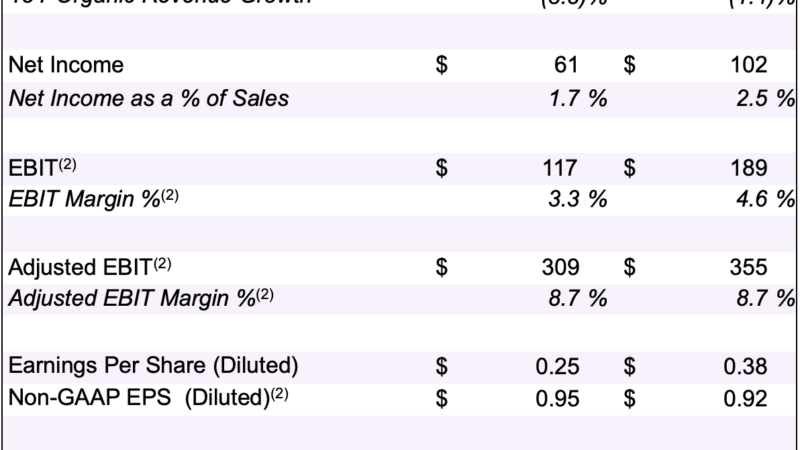

Ken will then discuss our financial results in more detail and provide our updated guidance. And finally, I will make some closing remarks before opening the call up for questions. In Q3, revenues were $3.57 billion, and our organic revenue growth was negative 3.8%. This was a direct result of the weak bookings in the first half of the year.

However, our organic revenue grew for the second consecutive quarter sequentially, and it is notable that we have driven the same level of revenues in constant currency, excluding dispositions for all three quarters in FY ’23. Our adjusted EBIT increased from 7.5% in Q2 to 8.7% in Q3, highlighting the strong execution of our cost optimization efforts while not negatively impacting our customers. Our non-GAAP EPS increased to $0.95. Our book-to-bill of 1.34 is the strongest book-to-bill result since I’ve been CEO.

This quarter, we almost hit on all cylinders by having five out of our six offerings deliver a book-to-bill of over 1.0 Overall, Q3 showed strong execution and has created good momentum for us. So, now let me give you some additional color around our transformation journey, which is at the core of how we are creating these results. The first step is to inspire and take care of our colleagues. We are seeing improved attrition due to the way we are taking care of our colleagues and our efforts to change the culture at DXC.

I am proud of how we are taking care of our roughly 4,000 colleagues in the Ukraine, and we continue to be impressed by their resiliency to take care of their families and our customers. Concerning COVID-19, we were just awarded the President Certificate of Commendation in Singapore. This prestigious honor has awarded organizations that made exceptional efforts, which had a significant impact in Singapore’s fight against COVID-19. I want to thank the women and men of DXC, along with my leadership team for their continued execution.

And as we look to ’24, we will continue to take care of our people and continue to adjust and add to my leadership team to deliver on our commitments. The next step in our transformation journey is to focus on our customers. The key metric here is our Net Promoter Score. And our most recent NPS score was 27, near the top end of the industry benchmark.

This solid customer delivery has driven sequential organic revenue growth in constant currency for two quarters in a row. The key thing I would like to highlight is that we have now delivered roughly the same level of revenue in constant currency, excluding dispositions for all three quarters in FY ’23, and you will hear from Ken that we are guiding to a fourth quarter at a similar organic level. Now, this is a great accomplishment as we have been a company with declining revenues for the past several years. Also, you will see our strategy for GBS and GIS working.

In GBS, we continue to grow the business and expand margins. This is the seventh quarter of consecutive organic revenue growth. As a result, GBS continues to become a larger part of DXC, now accounting for approximately 49%, up from 48% in Q2, demonstrating that the business mix is trending toward the new tech of GBS. In GIS, we continue to stabilize revenue and expand margins.

We are seeing our increased financial discipline and ITO payoff as the demand we saw in the market translated into strong bookings this quarter, which we expect to drive future revenues. So, you can see we are executing on both parts of our growth strategy to accelerate growth in GBS and moderate the declines in GIS. This execution of our growth strategy is why we expect to drive flat to 1% organic revenue in FY ’24. The third step is to optimize cost.

Clearly, we are executing on our cost takeout numbers as we expanded our margins from 7.5% in Q2 to 8.7% in Q3. We continue to take a thoughtful approach to cost takeout by focusing on our entire organization while delivering for our customers. This approach gives us confidence that we can continue our efforts for the remainder of FY ’23 and into FY ’24. The other piece of our cost optimization efforts is portfolio shaping.

You will hear from Ken that we were able to generate approximately $375 million of cash from the sale of data centers in the quarter, along with the German banks in early January. In the area of seize the market, I am extremely pleased with our bookings this quarter. A record book-to-bill of 1.34 brought us back to over 1.0 on a year-to-date basis for FY ’23, and this shows strong momentum as we are completing FY ’23 and heading into FY ’24. In GBS, all three offerings delivered a book-to-bill of over 1.0, and we continue to see momentum in our engineering and software capabilities that we discussed last quarter.

But this quarter, we saw even greater success in applications. In GIS, our more disciplined approach to dealmaking has paid off. In Q3, we signed over $800 million of ITO deals that were delayed from the first half of the year and signed two new logos by closing deals with SAP and Yard Fisher and Modern Workplace. Again, this shows good execution and momentum as these deals will create future revenue.

It is clear that there is demand in the market for our offerings, and we need to be patient because we are taking work from our competition at better economics. Our final step is our financial foundation, where we generated $463 million of free cash flow this quarter. The execution in this area was outstanding, and it gives us great momentum to hit our yearly guide for free cash flow. This free cash flow result, along with the cash we generated from portfolio shaping, including the sale of the German banks in January, totaled $840 million.

We anticipate that we will use approximately $400 million to pay down our debt, further enhancing our investment grade profile. And we plan to repurchase approximately $400 million of DXC shares to complete our previously announced $1 billion share repurchase program. Now before I turn the call over to Ken, I want to reiterate what we said in our October 4 press release. Management has been approached by a financial sponsor regarding a potential acquisition of a company.

Consistent with our fiduciary responsibility to maximize shareholder value, the company is engaged in preliminary discussions and is sharing information. We do not have any further update on this situation today, and we will not be commenting on it further. Now let me turn the call over to Ken.

Ken Sharp — Executive Vice President and Chief Financial Officer

Thank you, Mike. Let me provide you a quick rundown of our Q3 performance. Q3 organic revenue declined 3.8%. Adjusted EBIT margin and non-GAAP diluted earnings per share were above the top end of our guidance range at 8.7% and $0.95, respectively.

Free cash flow was $463 million in the quarter. The team is making great progress with what we expect will be two consecutive years of positive cash flow of at least $630 million. This is quite a turnaround from two years ago with over $650 million of negative free cash flow. Moving to our key financial metrics.

Third quarter gross margin declined 60 basis points on lower volumes. SG&A as a percent of sales increased 10 basis points. Depreciation was lower by 10 basis points. Other income increased 60 basis points, primarily due to asset sale gains of $24 million and FX hedging gain of $11 million, partially offset by lower pension income.

As a result, adjusted EBIT margin was flat compared to prior year and up 120 basis points sequentially. EPS was up $0.03 compared to the prior year due to $0.08 from a lower share count, $0.06 from a lower tax rate, $0.02 from lower interest expense. These benefits were partially offset by $0.13 from lower revenue and FX. Let’s turn to our segment results.

Our business mix continues to improve as our GBS revenue mix increased 110 basis points to 48.7% of DXC’s revenue. GBS grew 0.2% organically. The GBS profit margin declined 220 basis points year over year and was up 130 basis points sequentially. GIS organic revenue declined 7.4%.

GIS profit margin increased 190 basis points year over year and was up 50 basis points sequentially, benefiting 80 basis points from settling a commercial matter in the current quarter. Turning to our offerings. Analytics and engineering continued with solid organic growth, up 11.7%. Applications declined 6.8% on lower project revenue, coupled with a difficult prior-year compare as Q3 was the strongest growth quarter in FY ’22.

Insurance, software and BPS is up 3%. Our insurance software business is about $550 million of annual revenue and grew approximately 7% in the quarter. Security was up 4.2%. Cloud infrastructure and IT outsourcing declined 5.4%.

Modern Workplace was down 15.3%. We are encouraged by the recent new logo wins. Let me tie the year-over-year organic revenue decline above with Mike’s earlier point on sequential quarterly revenue. I am pleased to note that we’ve delivered three quarters of revenues that are flat on a constant currency, excluding divestitures basis.

Further, we are guiding to a fourth quarter that is also going in a positive direction, all while on the backdrop of very strong Q3 bookings, demonstrating our momentum. Turning to our financial foundation. Debt is $4.7 billion. We continue to tightly manage restructuring and TSI expenses.

These expenses totaled $55 million in the quarter. And year to date, restructuring in TSI is $147 million, down $124 million from prior year. Capital expenditures and capital lease originations as a percent of revenue were 6.4% in the quarter, up 120 basis points as compared to prior year. We continue to believe our capital intensity presents a long-term opportunity to improve cash flow.

Free cash flow for the quarter was $463 million on January 3. We closed the sale of our German banks. Customer deposits were $70 million lower as compared to the start of the year, thus creating a free cash flow outflow. With the sale of our German banks for EUR 300 million, we have substantially completed our $500 million portfolio shaping and asset proceeds goal.

Last quarter, we announced a new $250 million asset sale proceeds goal. While selling these real estate assets will bring in real cash, we expect to incur a noncash loss that is not incorporated in our guidance. In Q3, we closed on four facility sales, yielding $56 million of cash proceeds, and recognized a $16 million gain. The combination of our Q3 free cash flow, sale of our German banks, and our Q3 asset sales delivered $840 million in cash.

To put a finer point on the $840 million of cash, it is over 12% of our market capitalization. We expect to deploy $400 million to repay a portion of our debt, and we’ll adjust our target debt level to $4.5 billion. With the bank sales, customer bank deposits are no longer part of our cash balance. Accordingly, we are reducing our target cash balance to $1.8 billion.

As these new target levels, we have an additional $400 million available to repurchase our stock. Turning to our capital allocation on Slide 19. We repurchased approximately $600 million of our stock to date. With cash on hand, we feel good about our ability to deliver on our $1 billion share repurchase.

Our Q4 guidance. Organic revenue decline of minus 2.6% to minus 3.1%. Adjusted EBIT margin of 8.7% to 9.2%, and non-GAAP diluted earnings per share of $1 to $1.05. Turning to our FY ’23 guidance.

Organic revenue decline of minus $2.6 million to minus 2.7%. Adjusted EBIT margin of 8% to 8.1%. Non-GAAP diluted earnings per share of $3.45 to $3.50. As I mentioned earlier, our free cash flow was negatively impacted by $70 million due to lower customer bank deposits held in our German banks.

Accordingly, free cash flow was adjusted to $630 million. As Mike and I reflected on our FY ’24 guidance we gave almost two years ago, we envisioned a business that could grow with solid margins and good quality cash flow. We still envision that same business today. Let me provide you some context on our original FY ’24 guidance.

At the time, organic revenue was declining double digits, and we guided to organic revenue growth of 1% to 3%. Adjusted EBIT margins were approximately 6%, including 190 basis points of noncash pension income, and we guided to a 10% to 11% margin. Free cash flow was negative $650 million, and we guided to $1.5 billion of free cash flow. Lastly, let us not forget the $900 million of annual reoccurring restructuring and TSI costs that we guided to $100 million, all while expanding margins.

From our vantage point, we have come a long way over the last two years as the business is on a much stronger foundation. Let me take a minute to update you on our preliminary FY ’24 expectations. For organic revenue, we are working plans to drive the business to flat to 1% growth, adjusted EBIT margin to expand above FY ’23 levels, but do not expect margins to exceed 9%. When we provided the FY ’24 EBIT guidance, pension income was 65 basis points higher than where we are in FY ’23.

We are assuming pension income continues at a similar level and is a 65-basis-point headwind from our original FY ’24 guidance. Free cash flow to increase above FY ’23 levels, but do not expect to exceed $900 million. When we set our FY ’24 $1.5 billion free cash flow guidance, we had $900 million of capital lease payments. The capital lease payments are not part of free cash flow, but we’re a significant consumer of free cash flow, leaving $600 million of cash generation.

As we sit here today, we expect to originate about $200 million to $250 million of capital leases in FY ’23. Our lower originations over the last couple of years have driven down the capital lease payments to about $400 million next year. We will refine our FY ’24 guidance on our next earnings call once we complete our annual planning process. With that, let me turn the call back to Mike for his final thoughts.

Mike Salvino — President and Chief Executive Officer

Thanks, Ken, and let me leave you with a key takeaway. We will achieve our inflection point at the end of FY ’23 and deliver the business we have always envisioned in FY ’24, albeit with slightly lower guidance. As we exit FY ’23, you can see that we have cleaned up many of the challenges from our past that Ken just outlined. Our clear execution of our transformation journey has built a quality company that you can depend on to deliver revenue that is not declining, change the mix of the revenue to the higher-value tech offerings of GBS, expand both margins and EPS, win new work in the market as our offerings are relevant and in demand, generate strong free cash flow, manage our debt and return cash to shareholders.

Now, this is great execution, but we didn’t come here to DXC to fix the challenges. With the momentum that we’ve created in the business, we have confidence that we are poised to deliver the business we had envisioned in FY ’24 as we can see the ability to drive revenue flat to 1% growth, expand both margins and EPS, rotate the revenue to the new tech of GBS and generate increased free cash flow. Getting this inflection point was no small task, and my management team and I are proud of the quality company we have created, along with being clear and excited about the future of DXC. And with that, operator, please open the call up for questions.

Questions & Answers:

Operator

[Operator instructions] Your first question comes from the line of Bryan Bergin with Cowen. Your line is open.

Mike Salvino — President and Chief Executive Officer

Hey, Bryan.

Bryan Bergin — Cowen and Company — Analyst

Hey, guys. How are you doing? Good afternoon. Thank you. Wanted to start on free cash flow.

So, Ken, just hoping to dig on the moving pieces here to make sure we understand this for ’23 and ’24. So, can you first talk about some of the factors that drove the strong 3Q performance? Should we expect the continued lumpiness in free cash flow generation going forward? Or does that start to kind of smooth out? And then just to clarify on the last point you made there, after capital leases, it sounds like the real net free cash flow difference in your fiscal ’24 post-capital lease payments is about $100 million, given you’ve taken the number down. So, a couple of combo questions are on free cash flow to start, please.

Ken Sharp — Executive Vice President and Chief Financial Officer

All right. Great, Bryan. And look, if I need to clarify, feel free to jump back in. Look, it’s great work from the team, right? We’ve been at this for a couple of years, right? If you wind the clock back, the business had negative free cash flow.

We’ve done a lot of work. Probably the biggest, you look at it now two years in a row of positive cash flow over $600 million. So, it’s really not lost on us, right? A lot of good work from a lot of people across the entire business. The biggest driver, right, if you had to just kind of look holistically at the business has been the focus on driving down the restructuring in TSI.

So, I think that’s been somewhere around $600 million swing, so year to year. So, I think that’s a pretty big piece. And then just this quarter, we had built up some AR. It’s a little bit hard to tell on the balance sheet but — because of FX movements and so forth.

But we had built up some AR in the last couple of quarters and brought that back down this quarter to kind of a more normalized level. So, really, the team has done a nice job just driving across the business. And then when you look to FY ’24, I think the net is a good way of looking at it. The leasing was out of probably a little bit — it didn’t have the right economics from our perspective.

So, when we looked at it, and it also creates some, I would say, business oversight challenges. When you’re leasing a lot of assets, it’s not always as economic as you want it to be. So, we went through a process of making sure that when you lease assets that it goes through kind of the right economics and has the right hurdles to it. So, when we did that, of course, we brought down the level of leasing pretty dramatically.

I think everybody knows this, right, but it gets a little confusing on the cash flow statement. If you lease assets, they drop below free cash flow because they are financing purchase basically. If you buy them straight out, they go rate through capex. So, as we squeeze down on the leasing, certainly that some of that capital ends in the capex, which directly impacts free cash flow.

So, in that way, is certainly a good way to look at it. I mean, certainly, I think when you look longer term, we’ve got opportunities to improve it. Our capex as a percent of revenue is higher than a lot of our peers, so I think that’s a place we need to continue to work on. And then your question around the lumpiness of the cash flow.

Q1 is always going to be a little bit, and I think most companies have this, right? There’s a lot of cash outflows that go through Q1. So, I think in the future, you’ll see that continue to be a bit more of a negative quarter. We’ll work at it. Q2, I think we’ve got some work to do to make sure that we level that out.

And hopefully, Q2 is more positive than this year. I think it was slightly positive, but like to keep working that. Q3 and Q4 always have been pretty strong cash quarter. So, we’ll keep at it.

Bryan Bergin — Cowen and Company — Analyst

All right. Thanks for taking the question. Yeah, please. Just on bookings and demand, Mike.

So, good to see the broad-based performance across the offerings. Can you talk about near-term pipeline now that you’ve gotten some of those larger deals over the line that you were holding back? And just any change in client sentiment and sales cycles and things like that, just given the macro?

Mike Salvino — President and Chief Executive Officer

Well, look, the client sentiment is pretty simple. The whole industry is focused on efficiency. It’s focused on cost savings. And what we’re seeing is that the deals will be larger, just like the $800 million number that we gave, and they’re taking a little bit longer.

The other thing that we’re seeing out in the industry is the fact that, look, customers are still focused on revenue, but it needs to be immediate impact. So, when I boil that all up and look at our offerings, I look at the ITO offering, there’s not going to be too many audit committees at these companies’ boards that will take that spend down. And the reason for that is because they don’t want any cybersecurity attacks. So, we’re still seeing demand for that offering.

The second is when you look at modern workplace, we’ve still got a lot of companies that are supporting a major, major part of their population, their employee base and a virtual mindset. So, you can’t really curtail that spend too much. And then when I look at the ability to drive revenue, that’s what our engineering business does. And I’ve said over and over again, we’ve got unique skills.

I continue to look at that business and see double-digit growth, along with a very solid book-to-bill. So, from a demand standpoint, it’s hard not to be cautious. But look, I mentioned on the last call that I’m adjusting the sales model. And I think focusing on what I call relationship selling in GBS, which means we go build the deep relationships and then sell our offerings based on strategic points of view that will either drive revenue or decrease cost.

And then look, the GIS business is always going to be there, and what we need to do is continue to win in the marketplace. So, I love the new logos, and I love the better economics. So, Bryan, that’s how I’d answer your question.

Bryan Bergin — Cowen and Company — Analyst

All right. Great. Thank you, guys.

Mike Salvino — President and Chief Executive Officer

Thanks, Brian. Brent, Next question.

Operator

Your next question comes from the line of Ashwin Shirvaikar with Citi. Your line is open.

Mike Salvino — President and Chief Executive Officer

Hi, Ashwin.

Ashwin Shirvaikar — Citi — Analyst

Thanks, Mike. Hi, Ken. Good evening and good to hear from you. Want to go back to free cash flow, but talk about deployment.

I see the deployment notes with regards to the immediate buyback paydown. Could you talk a little bit more granularly about the timing of those? And it was interesting to see that tuck-in M&A was not specifically noted. Basically, what are you probably thinking as it relates to ongoing deployment of free cash flow?

Mike Salvino — President and Chief Executive Officer

OK. So, why don’t you take the immediate? I’ll take the long term.

Ken Sharp — Executive Vice President and Chief Financial Officer

Sure. It sounds good, Mike. So, just, Ashwin, on the timing, we put out a $1 billion commitment on the share repurchase. And I think our perspective, that kind of looks like the end of this fiscal year when we file the K.

So, ideally, that would be the kind of ballpark timing we would hit. We always like to deliver on our commitment. So, we’ll work at that. It always depends on what the share price does, volumes, and all those things.

Because as you know, repurchasing shares, it’s highly regulated, and there’s processes you need to follow. So, we’ll do that in good stead, so we should be in good shape. The debt retirements, I think you’re also asking about, we just — we like to run somewhat fiscally conservative. We like to keep our leverage ratios in line.

So, we have some European commercial paper. It’s relatively short duration. There’s no cost to take it out, so we’ll reduce that. We’ve got also some preferred stock that’s a little bit higher yield that it’s a mandatory redeemable.

It also comes up at the end of the quarter. So, we’ll clean that up and be in good shape. We do tend to keep a little bit of a cash buffer as well. So, to the extent Mike wants to do some tuck-in M&As, we’ve always kept some reserves in one hand.

So, I’ll let — I’ll turn that to Mike for the remainder part.

Mike Salvino — President and Chief Executive Officer

So, Ashwin, in terms of capital allocation moving forward, what I would say is focus on that inflection point. I made the inflection point about us getting to the end of FY ’23. What you see is the revenues now aren’t declining. We’re definitely changing the mix of our business to GBS.

We’re expanding our margins and EPS, and we’re generating good quality free cash flow. So, as I look into ’24, one of the things that we’ll be discussing here is it feels like it’s time to start looking at the tactical tuck-ins. My two favorite slides in this deck are 15 and 23. And if you look at 15, you see the stability of the revenue.

We basically are now in the same amount quarter after quarter after quarter. So, now it’s a matter of let’s look at the new bookings, let’s look at the things that are potentially complementary to our business. And then when you look at Page 23, you can see the challenges that we’ve come through. When we talk about the quality company, you can see how we measure that, and then you can also see how we’ll take the thing forward.

So, there will be some balance to the capital allocation. I’m not ready to say one way or the other. We’re going to get through our ’24 planning, but we’ve gotten to that inflection point, where I do think it’s time to start considering that. Do you have a second question, Ashwin?

Ashwin Shirvaikar — Citi — Analyst

All right. Yes, I do. Thank you. So, investors are obviously very interested in revenue visibility, and you’re guiding to not just obviously the next quarter, but you gave initial outlook, new initial outlook for fiscal ’24, so speaking 15 months out.

And I just wanted to ask you to kind of comment on your visibility sort of in terms of the bookings you had, but also the pipeline replenished, the segment level granularity that you’re seeing, the model going forward, if you could comment on that.

Mike Salvino — President and Chief Executive Officer

OK. So, look, in terms of the visibility, there’s nothing better than seeing that revenue being stable. So, we’re not fighting a lot of the challenges around customers, around terminations, around that sort of stuff. That’s why I give you all the NPS number each quarter, which again is at 27.

And we’re doing that on the back of also continuing to expand our margins. So, when I look at that stability, that means step 1 should be completed. I mean we’re not going backwards anymore, so now it’s time to go forward. So, we feel pretty comfortable that the revenues will be stable.

Love the fact that, that book-to-bill came in at 13.4. We didn’t deplete the pipeline. I expect to continue momentum into Q4, and you start stacking up a few more quarters. And Ashwin, I think we’re going to be right where we wanted to be.

So, that’s how I’d answer that question.

Ashwin Shirvaikar — Citi — Analyst

Great. Thank you.

Mike Salvino — President and Chief Executive Officer

Brent, next question.

Operator

Your next question is from the line of Bryan Keane with Deutsche Bank. Your line is open.

Mike Salvino — President and Chief Executive Officer

Hey, Bryan.

Bryan Keane — Deutsche Bank — Analyst

Hey, guys. How are you doing? I kind of had a follow-up on that one on Ashwin’s question there. Because I guess in its history, Mike, DXC has had trouble getting to that inflection point. And we’ve heard it from multiple management teams over the years that we’re going to see the inflection point, and it just has never come.

Maybe you can just talk about —

Mike Salvino — President and Chief Executive Officer

You’ve never heard that from me, so the fact that I’m mouthing that is a pretty big deal.

Bryan Keane — Deutsche Bank — Analyst

Yeah, and that’s what I’m trying to get at here because it feels a little more real this time. Because in its history, it hasn’t been able to do it, but it sounds like maybe with fixing the troubled contracts and fixing the mix of business that we’re finally at a point that the visibility is strong enough that you feel confident this can be a positive organic growth, not only next year, but just from years to come.

Mike Salvino — President and Chief Executive Officer

Yeah. I mean, Bryan, look, here’s what I see. And again, we went — we focused on putting 15 in for a reason. OK.

And you guys can see all the adjustments that Ken and I talk about in terms of FX and disposition and so forth. But when you look at ’23, the biggest thing we will have achieved is customers that count on us, stable revenue that is not declining and the change of mix. We’re almost at 50%, which is all stuff that when Ken talked about how we envision the business two years ago. This is where we wanted to be.

So, the reason why we kept saying that, hey, we’re also guiding toward a fourth quarter at about the same revenue, that’s a clear indication that as we flip to next year, if we continue to keep the book-to-bill and when I look at book-to-bill, again, I know we had a great quarter, 1.34, but the trailing 12-month book-to-bill is what I’m looking at, that 1.06 that increased. That’s good stuff. The other thing that’s good stuff is literally looking at the individual offerings. OK? So, if I go to the businesses first, GBS and GIS.

GBS grew for the seventh consecutive quarter. The point to, there was a tough compare there. We did do a perpetual software sale of about $36 million last quarter. I totally expect that business to be back up around three in Q4.

Then when you look at our strategy for GIS, it’s awesome. The fact that we are literally taking our time with these deals, the deals are out there, I can now stop talking about and we could show you guys the results. $800 million is a big basket of deals at better economics. So, when I talk about the clarity and the excitement of DXC, you’re leaning into what you should feel now because I meant what I said.

You’ve never heard me say, all right, flat to one within a very short time frame. And look, I mean we’re pretty happy about the fact that two years ago, we called one to three, and we’re still looking at that one pretty closely. So, Bryan, do you have a second question?

Bryan Keane — Deutsche Bank — Analyst

Got it. Yeah. My second one is just on the — I know you can’t comment about what’s going on with the strategic kind of review. But usually, these things take one or two months.

This one seems to be taking longer. I’m just curious why the length of period. And I’m a little concerned, does it have any impact on the business fundamentals, the length of the review?

Mike Salvino — President and Chief Executive Officer

I mean, look, I reiterate we won’t comment on any further. I mean, look, the press release still stands. That confirms that we’re still having discussions. And Bryan, that’s about all I’m going to say.

Bryan Keane — Deutsche Bank — Analyst

Anything on the — has it hurt anything in the fundamentals of the business, the review? Or do you think that’s not been —

Mike Salvino — President and Chief Executive Officer

No, not at all. I mean there’s no way you can go expand margins, increase GPS or EPS, drive the free cash flow and book 1.34 if it was really having a big problem.

Bryan Keane — Deutsche Bank — Analyst

Got it. Thanks so much.

Mike Salvino — President and Chief Executive Officer

All right. Thanks, Bryan. Brent, next question.

Operator

Your next question is from the line of Darrin Peller with Wolfe Research. Your line is open.

Mike Salvino — President and Chief Executive Officer

Hi, Darrin.

Darrin Peller — Wolfe Research — Analyst

Hey, guys. Thanks. Hey, Mike. It’s good to see the momentum on this, the trajectory you guys have been showing.

I guess I just want to sort of circle back to a couple of the answers you gave on whether it’s the question Bryan which is asking or the question around M&A. But broadly, I mean is the portfolio that you have now, Mike, the right portfolio of assets for the next few years for DXC, I mean I know you mentioned some tuck-ins. But anything else to divest? And then really, where are you focused from a tuck-in standpoint if you’re going to make some moves? Or are we going to just digest what we have now and let the company operate and see if we can execute toward those fiscal ’24 targets?

Mike Salvino — President and Chief Executive Officer

Well, I mean, look, I think it’s a combination of all those. And what I would tell you is with where the market is right now, there should be some pretty good buys. If we did do anything, we would do it in GBS because what we’ve been saying the whole time is we need to change our mix, change our mix. Now having said that, I’ve also said over and over again that the GIS business can be a good business for us, and we do think that can produce good cash for us.

So, when I look at it, there is now a part of me that you know my past history that I did a tactical tuck-in in seven years. So, now in terms of stuff that we are continuing to look at, you’ve now heard Ken say, for two quarters that we have $250 million of data centers and facilities that we’re going hard after, and we sold a few this quarter, so we will keep doing that. The next thing is I look at countries in terms of this is still part of what I would call the cleanup, meaning I think we’re in too many countries that we, quite frankly, shouldn’t be in. There’s not a real strategic reason that we need to operate, but that was nothing more than taking HP and CSC and putting it together, and we can finally go after that.

And then there’s still a few other businesses, like the Dynamics business that we still would like to move on. So, look, you’ll see, I think, a whole combination of those things, Darrin. I mean we’re certainly not done. And I think what you’ve seen in us is we’re not going to wait around.

We’re going to continue to be aggressive with the business because we do think it’s got a lot of merit. We do think we’ve got more clarity in terms of what we see now, and I think we can get more focused on some of the last few things that we need to clean up. Darrin, you got a second question?

Darrin Peller — Wolfe Research — Analyst

I do. It goes back to the demand discussion that somebody asked earlier. I guess the bookings, obviously, some of it was, like you talked about, last quarter, pulling into this quarter, flowing into this quarter, which helped. But can we just revisit that for a minute in terms of what you’re seeing in terms of what kind of projects are looking like they’re winning bookings now? Because the book-to-bill ratios are strong in both GIS and in GBS this quarter, even like you said, even modern workplace.

I think you talked about having — it was great to see the new logos. So, can you give us a sense of what you’re actually seeing and if there’s been a change in sentiment on demand from the enterprises that you’re working with?

Mike Salvino — President and Chief Executive Officer

OK. So, I’ll take each offering individually. So, what we’re selling in A&E is engineering. And a lot of our engineering projects are in automotive, and we still see quite a bit of demand in banking.

And a lot of that stuff is analytics around. Also, can we help a customer generate new revenue? So, that’s what we’re selling there. So, think of projects, they’re smaller, but they’re quicker to generate revenue. In applications, what we’re doing with there is we’re dealing with custom apps.

So, think of something I’m building from the ground up. And then we’re also seeing ServiceNow, and we’re seeing SAP. And then in insurance, Ken mentioned the insurance software business Look, we’re right at the heart of a lot of the insurers because that software enables an insurer to write new books and business. So, the fact that that’s growing 7%, we’re not only selling the software.

We’re implementing it Darrin, and we’re also running it. Then if you drop down into GIS, there’s always going to be security projects. So, that 4.2% growth you saw this quarter is kind of nice. And then ITO is making sure that these infrastructures that haven’t moved to the cloud and then the ones that have moved to the cloud are basically, let’s call it, bulletproof.

So, that’s what we’re seeing, is the maintenance fee upgrades to that — those environments so that they don’t tip over. And then modern workplace. I think you’ll see that our uptime product is doing very well in the market. For SAP to have gone with us is a big deal.

They kind of know one or two things about software. So, that’s what we’re seeing, Darrin. Look, I wish that I could be more clear that the sentiment that’s out there that I read after every single one of my competitors’ earnings calls is that the thing is going to go backwards. But showing up with a 13.4 and saying that, look, it may be a little bit lumpy, but we still see very good demand for our services in the market.

So, to go back to the last point of your first question. Do I think DXC has everything it needs to have to take this thing into the future? We definitely have a good foundation. I would tell you that. We’ve got more than enough to make this a very good technology company.

And like I said, I like Page 23. It can literally show you the course that we’ve been on in terms of fixing the business, getting to a quality business and now where we’re going to go.

Darrin Peller — Wolfe Research — Analyst

Yeah. All right. That’s really helpful, Mike. Thanks.

Mike Salvino — President and Chief Executive Officer

Thanks, Darrin. Brent, next question.

Operator

Your next question is from the line of Keith Bachman with BMO. Your line is open.

Mike Salvino — President and Chief Executive Officer

Hi, Keith.

Keith Bachman — BMO Capital Markets — Analyst

Yes. Thanks. A good segue — Hi. Good afternoon or good evening, excuse me.

I did want to drill down on modern workplace a little bit. It’s a small part of your revenue, but it’s still over a point of drag on growth. And how does that shape out over the next one to two years? Can you get that to flat? Or what happens? Because it still is, frankly, a drag.

Mike Salvino — President and Chief Executive Officer

OK. So, Keith, let me give you the exact numbers because if you go back to Page 15, modern workplace mimics a lot of the overall business. So, if you look at the revenue for Q1, it was 447. If you look at the revenue for Q2, it’s 436.

If you look at the revenue for Q3, it’s 433. So, that thing has basically stabilized out. Meaning remember, when I put the business up for sale, we lost a number of contracts because why are you going to go with somebody that’s potentially going to sell the business? So, I think we’re through that puzzle piece. The fact that, like I said, we’ve got good new logos coming our way.

I think in Q4, you’re going to see a pretty significant change in that negative 16, 15 that we’ve been showing for the entire year. And then I do think we can get that business to flat to grow. So, hopefully, those numbers help.

Keith Bachman — BMO Capital Markets — Analyst

Yeah, it makes sense. And then I wanted to try to ask visibility a little bit differently. But in terms of the pipe, as we’re progressing over the next couple of quarters, how should we be thinking about the book-to-bill? I mean this quarter was obviously pretty strong. You focus on the latest 12 months.

But anything you want to call out as we think about the next couple of quarters on book-to-bill that will give us confidence that, that 0% to 1% growth is not only attainable but sustainable?

Mike Salvino — President and Chief Executive Officer

Well, Keith, think of it this way. I’m literally guiding to minus 2.5 to minus 3 in Q4. So, that should suggest that the demand that I just knocked down is going to show up, all right, sometime in ’24. OK? So, especially with the new logos and modern workplace, those are not project-type things.

That’s outsourcing-type work. The second thing I would tell you is having the business hit on all five out of six offerings shows that, look, we still have not only relevancy in the market, but there is demand. So, look, can I tell you what’s going to happen to the economy? I mean you look at everything. You read the scripts.

People say this is the year of efficiency. We do efficiency well, Keith. So, if people want cost savings and if people want somebody to run something efficiently, that’s us. So, like I said, I can’t call out exactly what’s going to happen.

And ’24 to three months or two or three quarters down the path. But what I can call is that we feel good about Q4, and we feel good about the momentum we’ve created so far.

Keith Bachman — BMO Capital Markets — Analyst

OK, Perfect. Many thanks. I’ll see the floor.

Mike Salvino — President and Chief Executive Officer

Keith, thanks. Brent, next question.

Operator

Your next question is from the line of Jason Kupferberg with Bank of America. Your line is open.

Mike Salvino — President and Chief Executive Officer

Hey, Jason.

Jason Kupferberg — Bank of America Merrill Lynch — Analyst

Thanks, guys. Hi, there. How are you? Thanks for taking the question. I just wanted to ask the first one on organic revenue growth.

I mean I know in the quarter, it was a little below plan. I guess fourth quarter is coming in a little below what was previously expected. So, just as you unpack that, I mean where would you say the shortfall has been relative to what you had previously anticipated? Which of the service lines?

Mike Salvino — President and Chief Executive Officer

It was modern workplace and applications. So, we expected that we would turn modern workplace quicker than we did because I kept telling everybody that that’s following the exact same transformation journey as ITO. You’ll see that we turned ITO within probably about a year. So, we thought we would turn that a little bit quicker.

And then applications, we expect it to get more project revenue out of that. When you looked at our plan for FY ’23, it was back-end loaded, and we expect it to get a little bit more out of apps. But I think apps will — you’ll see a turnaround in apps, just like you’ll see a turnaround amount of workplace in Q4 based on the bookings we just knocked down.

Jason Kupferberg — Bank of America Merrill Lynch — Analyst

OK. And then my second question was just more of a clarification, I guess. Ken, I think you said in the script that there was some kind of commercial matter that was settled that, I don’t know if I got this right, so correct me if I’m wrong, helped GIS margins by 80 bps in the quarter. Is that what it was? And is that just kind of a one-off?

Ken Sharp — Executive Vice President and Chief Financial Officer

Yeah. It’s kind of a nonrecurring. So, that’s why we called it out, but you got the numbers right.

Jason Kupferberg — Bank of America Merrill Lynch — Analyst

OK. So, what is that about 40-ish basis points overall or it was $80 for GIS.

Ken Sharp — Executive Vice President and Chief Financial Officer

Thereabouts, yeah.

Jason Kupferberg — Bank of America Merrill Lynch — Analyst

OK. Thank you, guys.

Ken Sharp — Executive Vice President and Chief Financial Officer

Yep.

Mike Salvino — President and Chief Executive Officer

Thanks, Jason. Brent, next question.

Operator

Your next question comes from Tien-Tsin Huang with J.P. Morgan. Your line is open.

Tien-Tsin Huang — JPMorgan Chase and Company — Analyst

Hey. Hi. Thanks for taking the question here. I just wanted to also hone in on the bookings side.

Mike, you talked about not depleting the pipeline, and demand is still good, but visibility obviously is driven somewhat by macro. Is there wiggle room if large deals slip or if project work gets pushed out for you to still see that inflection that you’re calling out here today? And also similarly, just want to better understand. You mentioned better economics, including on competitive takeaways. I’m a little surprised by that given the cost focus of clients.

So, just curious on what’s changed there, if you don’t mind elaborating on those two things on bookings. Thanks.

Mike Salvino — President and Chief Executive Officer

Tien-Tsin, thanks for coming on my call. It’s good to hear your voice.

Tien-Tsin Huang — JPMorgan Chase and Company — Analyst

Glad to be on.

Mike Salvino — President and Chief Executive Officer

Absolutely. OK. So, back to your questions. in terms of — which one do you want me to go to first?

Tien-Tsin Huang — JPMorgan Chase and Company — Analyst

Either one that’s easier. I kind of rambled a little bit. Just thinking about the wiggle room, maybe starting with that and even if things get pushed out a little bit maybe on larger deals or project work, for example. It sounds like you had a good backlog.

You feel good about the fourth quarter.

Mike Salvino — President and Chief Executive Officer

Hundred percent, let me start with that one first. So, when you think about wiggle room, I mean look at what we’ve done on the revenue on the back of 0.83 million and 0.87. So, when I look at that 12-month trailing book-to-bill, I can go all the way out five quarters, 0.92, 1.2, 1.2, 0.87, 0.83. Why am I doing this for you? There is wiggle room, OK, in terms of us making sure that we can sustain that revenue.

OK? And like I said, the 1.34 is nice because that means that we’re going to be executing against all that bookings come Q4 and then into FY ’24. So, the backlog doesn’t have to be perfect for us to get to that flat to 1% guide. Does that make sense, Tien-tsin?

Tien-Tsin Huang — JPMorgan Chase and Company — Analyst

It does. It does. It’s important to go back to those. Yeah.

Mike Salvino — President and Chief Executive Officer

And then your second question was —

Tien-Tsin Huang — JPMorgan Chase and Company — Analyst

The better economics, Mike, I think you mentioned, including on the takeaways.

Mike Salvino — President and Chief Executive Officer

No. This is clear. So, when I say that, it’s ITO. OK? And if you think about what’s happening in the space, our competition is struggling a bit.

And what’s interesting about the market right now is I remember those days. So, when I took over DXC, we were the ones that were struggling in terms of customer satisfaction, in terms of our balance sheet, in terms of our free cash flow, all that stuff. And if you go back to ’23, that’s not where we’re at anymore. All right? And I’ve talked on numerous calls that we’re now the safe pair of hands.

All right? And you’re talking to a CEO that literally likes the GIS space. All right? And as always said, that is key to what we’re trying to get done because we do think it can generate cash. OK. Now here’s the second piece.

When those deals that we’re looking at, Tien-Tsin, were done five, 10 years ago, that ITO space was a commodity space. It was a race to the bottom in terms of pricing. And we’re not — when those clients call us now, whether we’re joint with one of those competitors in a large client or it’s a brand-new logo, we are very clear about the economics that we’re going to do. One of the things that I talk about is going to infrastructure light.

That means we definitely get cola, that means we pass on things like electricity. We pass on things like hardware upgrades. We pass on things like software increases, And Tien-Tsin, you knew that was the playbook that I ran us the old place. So, when I say better economics, that’s exactly what we’re doing.

It’s taken me a little bit longer than I wanted to, to get there because we had stabilized a lot of delivery, but I like where we’re at.

Tien-Tsin Huang — JPMorgan Chase and Company — Analyst

Yep. No. Makes perfect sense. Appreciate your thoughts.

Mike Salvino — President and Chief Executive Officer

All right, Tien-Tsin. Thanks. Brent, let’s take one more question.

Operator

Your final question comes from the line of Rod Bourgeois with DeepDive Equity Research. Your line is open.

Mike Salvino — President and Chief Executive Officer

Hey, Rod.

Rod Bourgeois — DeepDive Equity Research — Analyst

Hey, guys. Hey, I have a question about bookings traction and a question about capital intensity. I’ll start on the bookings side. Your booking strength in the December quarter was pretty disconnected from less good trends in the broader IT infrastructure services market.

So, I want to ask, how much of your recent booking strength was due to push-outs from earlier in the year versus a real inflection point in your market traction? And if you are seeing a real inflection point, can you share more about what’s enabling that inflection point?

Mike Salvino — President and Chief Executive Officer

OK. So, first, I’ll talk about the bookings. So, if you take out the $800 million that we said was basically caught up in the first half of the year, we’re still at a book-to-bill of 1.12. So, that’s just the math.

That’s a very strong quarter. Also, the way I look at it, Rod, is we’re back over 1.0 year to date. So, you can look at it that way. You can look at it the trailing 12 months.

increasing from 1.04 to 1.06. Either way you look at it, the demand was good, OK, which, this is where I keep going back to. We do, all right. see not only the demand.

But we also — there’s a need for our services out there. That’s what I just keep coming back to. Now what we’re not going to do is race to go do some book-to-bill just to do the book-to-bill. Because on the GIS piece, we talked about our discipline over and over again that we’ll get that at the right economics.

And then look, I really like what we’re doing in GBS. When you look at all those offerings, 1.32 book-to-bill in apps, 1.15 and A&E, 1.06 in raise insurance business, that’s all goodness. So, Rod, what was the second part of your question again?

Rod Bourgeois — DeepDive Equity Research — Analyst

Yeah. Well, it relates to the disciplined topic in the GIS business. So, maybe it’s a good topic to end on. Capital intensity in the business is something that has been wrestled with here for years.

So, can you talk about the levers you have to get capital intensity down while you’re also achieving better revenue stability in GIS?

Mike Salvino — President and Chief Executive Officer

Ken, do you want to take that?

Ken Sharp — Executive Vice President and Chief Financial Officer

Yeah, sure. Yeah. No, Rod, we’ve been — this goes back to our whole governance process. We’ve put a thoughtful approach around free cash flow, cash generation on deals.

And as Mike said, it just takes time to work its way through the system. That’s probably the first part. And then your comment about historically, I think there wasn’t this cash culture and putting that in place, and part of the business came out of a hardware business. So, I think their desire to refresh and not really kind of manage capex like we need to, we just need to keep working that, right? So, we’ve even put some tools in place, which are going live this quarter to better forecast, manage, create accountability, tie back to the commercial team that Mike has been building out, which I think will be a big part long term.

I mean our focus is absolutely to support our customers, but we also need to make sure we’re getting a proper return on the business. And when you look at the capital intensity and the margins in the GIS space, you could easily argue we’re not giving right returns. So, we’ll keep sharpening the pencil there and drive our way down through it. But there’s certainly an opportunity to make headway there.

And if you look at our peers, right, you kind of quickly get back to the GIS space, ought to be somewhere around 5% of revenue, maybe 6% on a bad day. And the GBS space ought to be kind of a 1% to 2%. So, on that thesis, right, there ought to be an opportunity to get the capex down to 3% to 4% with a little bit of work, and that’s what we just need to do, and we need to keep adding.

Mike Salvino — President and Chief Executive Officer

So, Rod, let me leave you with these comments. When I look at that space in the three-plus, three and a half years I’ve been here. We first talked about is there even a need for that business that works, that infrastructure work. And I gave you all data that said, hey, that stuff is not going to go away.

Not everything is going to go to the cloud because all of our competition is always talking about the cloud, the cloud, the cloud. All right. Second is nobody liked that business because it was commodity. All right? So, a lot of people could do it, and that meant a race to the bottom on price.

OK. So, now where are we today? All right? There’s definitely a need because not all of the mission-critical stuff has gone to the cloud. All right. Some of it has, some of it hasn’t.

Second is the industry isn’t as commoditized as it once was because we’ve got competition that’s falling off. All right? So, therefore, us being there, right, to take the business, to make sure that we can deliver on what we said we were going to do is huge to get better economics. Now the last thing I will say is Ken was being very detailed. I would add to his detail by saying using our balance sheet to do deals is not something that we want to continue to do over and over and over again, and I’ll just leave it at that.

Rod Bourgeois — DeepDive Equity Research — Analyst

Got it.

Mike Salvino — President and Chief Executive Officer

So, Rod, did you have a second question or should I wrap the call up?

Rod Bourgeois — DeepDive Equity Research — Analyst

I think it’s time to wrap. Thanks, guys.

Mike Salvino — President and Chief Executive Officer

All right, Rod, thanks so much. Look, I appreciate everyone joining the call. Also, I want to thank everyone for joining the call. Some of you have made the time for DXC this quarter, and I do really appreciate it.

What I would end with is this. We definitely have both execution, and we’ve created great momentum in our business to get to what I think the inflection point will be at the end of FY ’23. And we expect to deliver like we had always envisioned the business in FY ’24. And we are very proud about the quality of the company that we’ve created, and we’re also very clear and excited about our future.

So, I look forward to updating you all in May. And, operator, please close the call.

Operator

[Operator signoff]

Duration: 0 minutes

Call participants:

John Sweeney — Vice President, Investor Relations

Mike Salvino — President and Chief Executive Officer

Ken Sharp — Executive Vice President and Chief Financial Officer

Bryan Bergin — Cowen and Company — Analyst

Ashwin Shirvaikar — Citi — Analyst

Bryan Keane — Deutsche Bank — Analyst

Darrin Peller — Wolfe Research — Analyst

Keith Bachman — BMO Capital Markets — Analyst

Jason Kupferberg — Bank of America Merrill Lynch — Analyst

Tien-Tsin Huang — JPMorgan Chase and Company — Analyst

Rod Bourgeois — DeepDive Equity Research — Analyst